World financial organizations have revised their near-term economic outlooks downward, cutting demand and putting pressure on OPEC to renew its supply cut agreement with Russia.

NATURAL GAS:

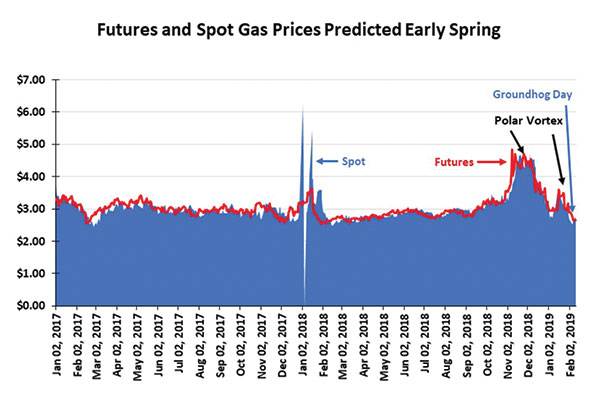

Punxsutawney Phil was rudely pulled from his hole by his handlers before dawn on Groundhog Day, but he failed to see his shadow on that February 2nd morning. Tradition says we are headed for an early end to winter. For those Americans in the Midwest and Northeast who had just suffered through their second Polar Vortex bone-chilling cold spell, Phil’s pronouncement was heartily welcomed. For natural gas prices, the second Polar Vortex in January had failed to boost them, as they further declined to unseasonably low levels, possibly in anticipation of Phil’s gray-morning debut.

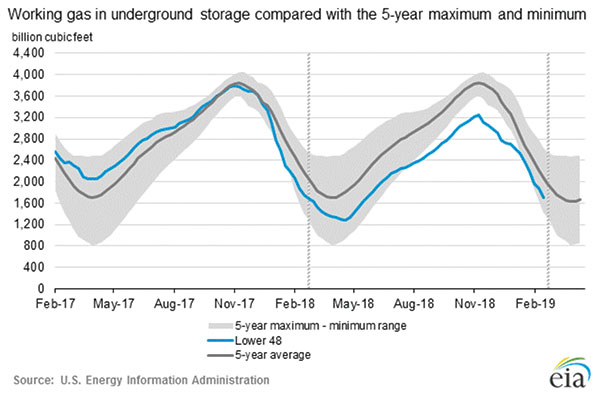

The early spring prediction weighed down gas prices despite several weeks of record gas withdrawals from storage required to help meet demand. Based on the latest gas storage data for the week ending February 15, there was 1,705 billion cubic feet of gas in storage, down 177 Bcf from the prior week. Storage volumes are 4.1 percent below a year ago and 17.9 percent below the 5-year average of 2,067 Bcf. As the chart shows, the current gas storage volumes have been tracking the 5-year average for the past few weeks, and is now within the range of maximum and minimum volumes over that period.

The early spring prediction weighed down gas prices despite several weeks of record gas withdrawals from storage required to help meet demand. Based on the latest gas storage data for the week ending February 15, there was 1,705 billion cubic feet of gas in storage, down 177 Bcf from the prior week. Storage volumes are 4.1 percent below a year ago and 17.9 percent below the 5-year average of 2,067 Bcf. As the chart shows, the current gas storage volumes have been tracking the 5-year average for the past few weeks, and is now within the range of maximum and minimum volumes over that period.

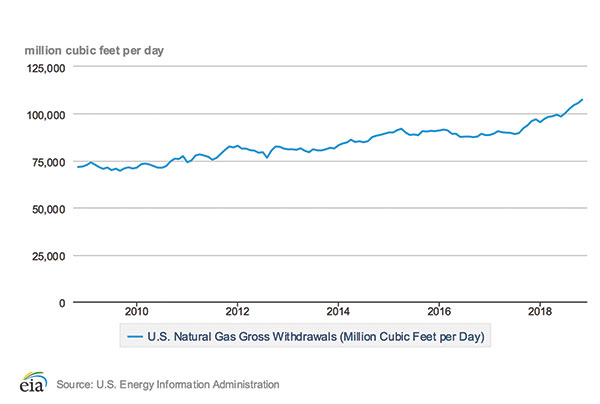

The latest data shows domestic natural gas production continuing to set new monthly records, reaching total gross production of 107.4 Bcf per day, an 11.7 percent increase over the last 12 months. The government is forecasting growth over the next 12 months of 3.7 percent, followed by a 1.5 percent increase the following 12 months. The problem with these forecasts is that the same agency predicted a 5.5 percent hike in output, when actual production grew 11.7 percent between November 2017 and the same month in 2018. This rapid supply growth, especially given the inability of the government experts to anticipate it, has convinced gas traders there will be no problem finding sufficient gas supply to rebuild storage volumes this summer in preparation for the winter of 2019-2020.

The confidence the gas market has about future supply is reflected in current gas futures prices. At $2.70 to $2.80 per thousand cubic feet, gas prices appear high enough to bring new supply on line to meet increased power consumption, satisfy residential and commercial demand, as well as deliver increasing volumes to LNG export terminals.

The confidence the gas market has about future supply is reflected in current gas futures prices. At $2.70 to $2.80 per thousand cubic feet, gas prices appear high enough to bring new supply on line to meet increased power consumption, satisfy residential and commercial demand, as well as deliver increasing volumes to LNG export terminals.

The increase in domestic gas output continues to confound experts who have predicted a slowing in supply growth due to the oil well drilling slowdown in regions with high associated gas volumes. While the supply and demand outlook will change one day, for the foreseeable future it looks as if natural gas prices will languish well below the magical $3 per thousand cubic feet price level and may even fall below the 2019 consensus expectation of $2.82 per Mcf.

CRUDE OIL:

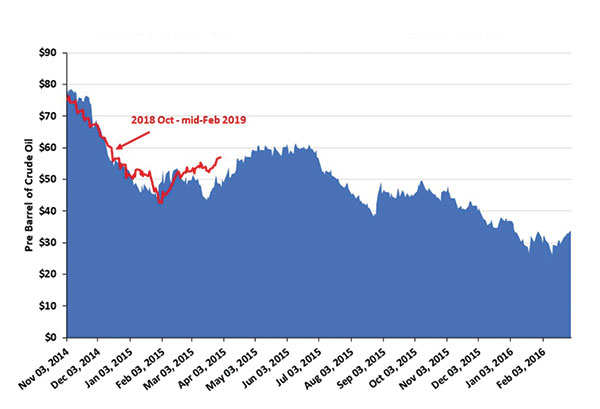

In contrast to the natural gas market, crude oil prices have been rallying since their recent low established on Christmas Eve. As WTI prices flirt with $57 a barrel, up over 20 percent since year-end, a degree of optimism has crept back into the oil community. Although oil-focused E&P company capital spending is projected to decline modestly in 2019 (-9 percent) from spending levels of 2018, current producer cash flows are higher than anticipated when managers planned their budgets during the fourth quarter.

Mid-February is too early to speculate on exactly how much of any additional cash flows may wind up drilling and completing more wells this year, as opposed to being returned to shareholders in the form of increased dividends and share buybacks. Preliminary indications by E&P companies who have reported 2018 year-end results and 2019 spending and production plans show a modest reduction in spending. But those declines were from budgets approved when the oil price outlook was questionable. A survey of E&P company executives attending the recent NAPE conference in Houston indicated that about 60 percent of them plan to spend all or more than their projected cash flow this year. So much for the fear of “capital discipline” restraining activity. The survey results are welcome news for oilfield service company execs who are fighting for business, which is needed to boost service prices.

Mid-February is too early to speculate on exactly how much of any additional cash flows may wind up drilling and completing more wells this year, as opposed to being returned to shareholders in the form of increased dividends and share buybacks. Preliminary indications by E&P companies who have reported 2018 year-end results and 2019 spending and production plans show a modest reduction in spending. But those declines were from budgets approved when the oil price outlook was questionable. A survey of E&P company executives attending the recent NAPE conference in Houston indicated that about 60 percent of them plan to spend all or more than their projected cash flow this year. So much for the fear of “capital discipline” restraining activity. The survey results are welcome news for oilfield service company execs who are fighting for business, which is needed to boost service prices.

The worrying issue for oil execs is that the current balanced oil market, which has aided the oil price rally, has been achieved primarily by supply cuts rather than rising demand. In fact, world financial organizations have revised their near-term economic outlooks downward, cutting demand and putting pressure on OPEC to renew its supply cut agreement with Russia for another six months following the June expiration. That supply cut has been helped by Canada’s mandatory production reduction, along with Venezuela’s continuing oil output contraction, and now U.S. economic sanctions. Without these cuts, and their likely extension through year-end 2019, oil prices would not be where they are currently.

For a sign of where crude oil prices may go in the future, watch the negotiations between Saudi Arabia and Russia. What those countries decide about their oil output will move oil prices. In turn, those countries are closely monitoring the health of U.S. oil shale production. Yes, there are lots of moving parts to track, but it is necessary in order to understand oil price trends!

For a sign of where crude oil prices may go in the future, watch the negotiations between Saudi Arabia and Russia. What those countries decide about their oil output will move oil prices. In turn, those countries are closely monitoring the health of U.S. oil shale production. Yes, there are lots of moving parts to track, but it is necessary in order to understand oil price trends!

By G. Allen Brooks | Author, Musings From the Oil Patch