Crude Oil:

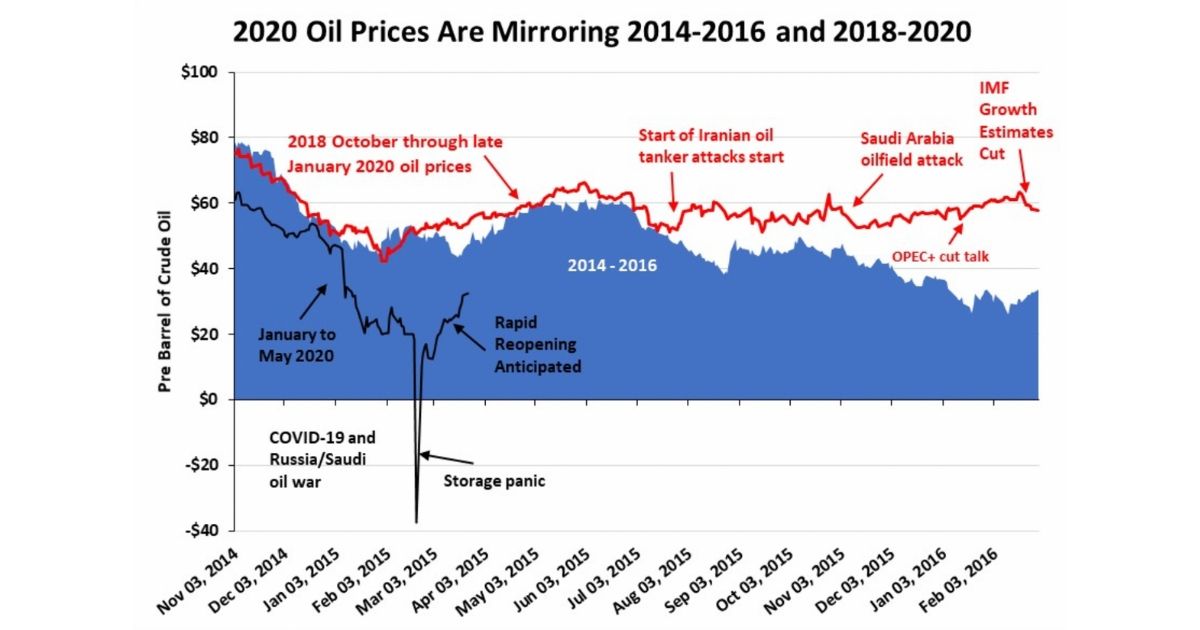

Barely a month ago, for the first time ever, crude oil futures traded at a negative $37 a barrel. Today, they are nearly $70 higher. From one of the worst collapses in oil industry history to one of the sharpest recoveries ever, crude oil price volatility has returned. Volatility creates opportunities for traders to make money, but in the real oil world, it creates operational and structural hurdles. Remember, today’s crude oil price is about $30 a barrel below year-ago prices, and even then, the industry struggled to generate profits.

The one-day oil price collapse was created by investors ignorant of their obligation at the contract’s expiration. When it ends, you must be prepared to take delivery of thousands of barrels of oil. At the time the contract expired, there was a panic over inadequate oil storage capacity. To the contrary, more storage appeared—and it wasn’t swimming pools, bathtubs or tankers.

The greatest oil price collapse impact was to force producers to stop drilling, and importantly, to shut in flowing wells, something thought unimaginable. Lost profits due to low oil prices could not be offset by producing more oil. With customers telling producers, “no más,” drastic changes were needed.

The greatest oil price collapse impact was to force producers to stop drilling, and importantly, to shut in flowing wells, something thought unimaginable. Lost profits due to low oil prices could not be offset by producing more oil. With customers telling producers, “no más,” drastic changes were needed.

The sharp oil price rebound has traders nervous. Prices have been driven up by the expectation for a rapid return to normality, meaning some semblance of pre-COVID-19 economic life. The scary issue is that some producers are reportedly turning Permian Basin wells back on. Will that upset the scenario for a rapid rebalancing of the oversupplied oil market? A recent analysis of government oil production data shows U.S. output may have already fallen by 25 percent—a drop of nearly three million barrels per day. Much more than anyone previously believed possible.

With new well economics destroyed, producers are stopping drilling and well completions. At the end of 2018, over 400 frac crews were supporting nearly 1,100 rigs drilling new shale wells. At mid-May, there were 70 percent fewer rigs working along with only 15 percent of the frac crews. And we may not have hit bottom.

Not many months ago, the industry would have been shocked to even contemplate $30 oil. Now they are almost giddy with oil at this level. While some forecasters believe prices have nowhere to go but up, given the cutback in oil company capital spending and sharply reduced activity, they may be ignoring the tidal wave of supply arriving due to the Russia-Saudi Arabia oil war. More cars on the road mean falling oil inventories, but 50 million barrels of Saudi oil arriving soon may overwhelm that improvement. Prepare for lower oil prices before they go higher.

Natural Gas:

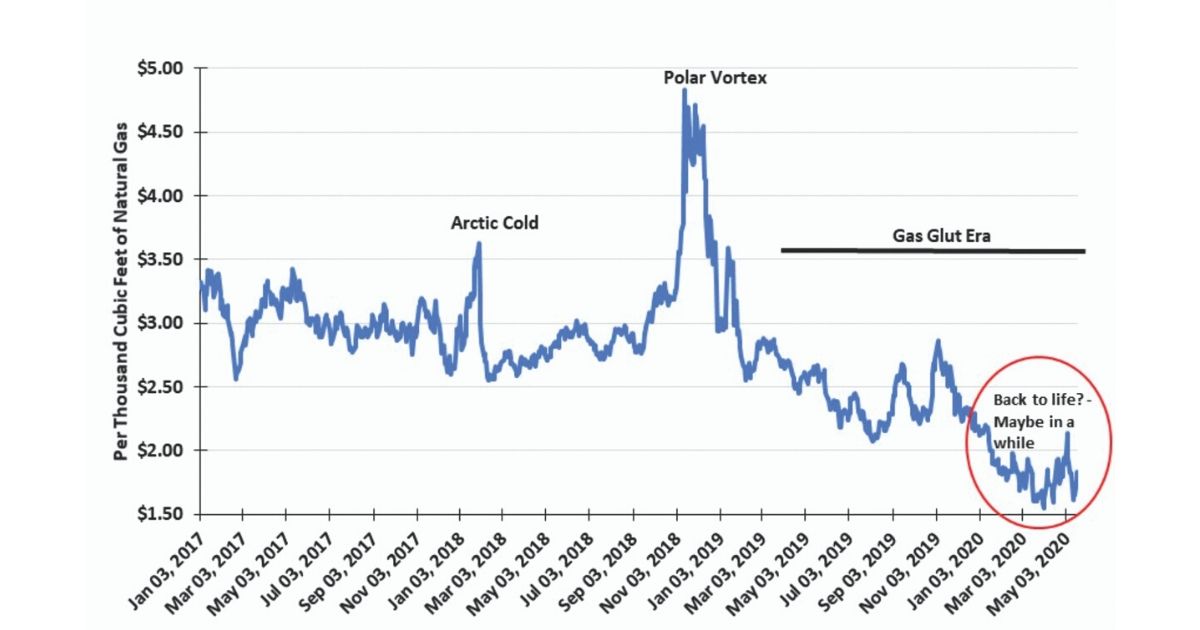

Natural gas prices are now primarily controlled by weather and LNG, but the oil price crash will affect gas supply. A sharp drop in associated natural gas from oil wells is a wildcard in the gas pricing equation. We have now entered the gas storage rebuilding phase of the annual industry cycle. How high temperatures climb this summer will influence the storage rebuilding pace. Hot temperatures equate to more air conditioning load and greater gas-fired power generation. More renewable electricity will provide some of that power, but summer temperature patterns often don’t match renewable supply peaks. Wind output is highest at night, which is why negative power prices often prevail then, as electricity companies must shed too much supply. Daily peak summer temperatures usually arrive in late afternoons, just as solar power’s contribution starts declining, leaving a supply/demand imbalance. These patterns are often upset by rainy days and still nights. Natural gas will continue to play an important role in the power generation business.

Tropical storm Arthur, which recently formed off the East Coast, is the first of what may be a significant number of storms this season. The tropical storm season runs between June 1 and November 30. Historically, 97 percent of tropical storms form in that period, with three percent occurring outside of it. While the early-forming Arthur is not unique, it is a wake-up call that gas markets might be upended this summer by storms.

The real story for natural gas prices is how quickly supply falls, as associated natural gas output declines due to lower oil production. At the same time, LNG demand is falling, a key component of demand growth over the past few years. Which supply and demand factor will be the most powerful gas price influencer?

Early reports suggest there may be a number of LNG cargoes cancelled in June due to weak European and Asian demand due to COVID-19. Europe has unseasonably high gas storage following consecutive warm winters and heavy storage fills last year, as the continent moved to protect against failure to renegotiate a 10-year gas supply deal with Russia. With additional gas pipeline capacity supplying European markets—Gazprom’s 3-Bcf/d TurkStream pipeline that commenced service in January, and the 1-Bcf/d Trans Adriatic Pipeline, currently in start-up mode—the possibility of a gas supply shortage this winter is low. Additionally, Gazprom’s delayed Nord Stream 2 pipeline should begin operating in early 2021. All of this supply makes LNG sales into Europe less attractive.

While China has resumed taking LNG cargoes, after declaring force majeure earlier this year during its COVID-19 shutdown, the abundance of cheap gas in neighboring markets makes long-distance U.S. LNG less appealing due to its higher transportation cost.

All of these market trends make predicting near-term gas prices a game of three-dimensional chess. A hot summer could help, but cooler weather might hurt. A rebound in oil prices might boost gas supply, just when lower associated gas supply is assumed. Dry gas output could rise in response to higher gas prices. Factor in an active Gulf of Mexico hurricane season, which could cut supply, or maybe damage demand. Lastly, the global economic reopening offers potential plusses and minuses to LNG supply and demand dynamics. The best guess now is for gas prices to struggle heading into the heat of summer.

By G. Allen Brooks | Learn more here.