Latin American Gasoline Imports Inch Higher in 1Q17

Latin American Gasoline Imports Inch Higher in 1Q17

PIRA projects 1Q17 Latin American gasoline demand to average 2.7 MMB/D, 15 MB/D higher year-on-year. Diesel demand is also expected to grow by 10 MB/D. Mexican gasoline demand is forecast to grow, while Mexican and Venezuelan combined demand of diesel is expected to be lower on the year. 1Q17 Latin American gasoline and distillate imports are projected to increase. Regional refinery runs are forecast down year-on-year. Brazilian refinery runs are expected to increase in the next few months as import incentives for automotive fuels are expected to limit imports. Petrobras raised its ex-refinery prices for both gasoline and diesel in December.

U.S. Ready for 2017 Call on Supply

Despite the ongoing inability to move gas optimally in Mexico, the nation’s dependency on Lower 48 gas will continue to increase in 2017, as domestic output of oil and gas is expected to remain on a protracted structural downtrend. Clearly, PEMEX’s ability to invest in exploration and production remains limited. Accordingly, with a large swath of cross border capacity set to commence in 1H17, Lower 48 gas should be primed and ready to fill such void.

PIRA U.S. Solar Market Outlook Sees Strong 2016-2021 Build, Limited Impact from Trump Administration

PIRA released a U.S. Solar Market Outlook examining major trends shaping the U.S. solar power sector, providing a five-year forecast of penetration (annual capacity build for both utility-scale and distributed systems) for key regions. Recent capacity installations, technology and system costs, policy and rate design, and other market trends are reviewed. Solar build is a key element of PIRA’s views and forecasts of North American Electricity power market balances and prices, and PIRA’s new U.S. Solar Market Outlook offers more detailed coverage of this key technology. PIRA forecasts strong build-out between 2016-2021 and does not expect substantial negative impacts on U.S. solar from policies under the Trump administration and 115th Congress.

Has the Fed Turned More Hawkish After Trump Surprise?

After the Fed raised the policy interest rate this week as expected, the focus is now on how often the central bank will tighten during 2017. The Summary of Economic Projections for December pointed to a somewhat more hawkish Fed. But projections have not yet incorporated possible effects from the incoming administration’s policy. Fed meeting participants remain in a wait-and-see mode, and the chance that the central bank will become overaggressive in raising rates next year appears low for now. U.S. data were encouraging this week. The Chinese government’s announcement on the car sales tax was positive for the vehicle sector outlook.

U.S. LPG Export Capacity Increases

Phillips 66 announced on December 16th that the Freeport, TX LPG terminal is fully operational, and has loaded its first contracted cargo on the 530-MB VLGC named the Commander. The terminal has nameplate export capacity of near 150 MB/D. The ship is headed to Cristobal, Panama but its final destination is likely China, via the Panama Canal. PIRA has observed that the terminal has been operating since mid-November and the company has loaded four VLGCs prior to the Commander. PIRA does not believe this facility will operate near capacity for sustained periods in 2017 due to expected challenging export arbitrage economics.

U.S. Ethanol Prices Soar

U.S. ethanol values were boosted by a robust export market and low inventories the week ending December 9. Assessments were supported by stronger corn and oil values. Margins jumped Friday. RIN prices tumbled after Scott Pruitt was nominated for Administrator of the EPA.

EUAs Will Be Trading on Policy Developments in 2017

After a Nov and early Dec where European carbon (EUA) prices traded in a wide €4.30-6.50 range, EUAs stabilized at €5 ahead of the EU Parliament’s European Committee vote on EU ETS post-2020 reforms – but moved down soon afterwards. EU ETS supply-demand fundamentals will remain poor in 2017, but policy developments could drive EUA prices. Positive post-2020 negotiations could offer some price support starting in 1Q17. However, progress on the EU’s 2030 efficiency and renewables targets will likely weigh on prices, although legislative schedules for those proposals have not been set.

Market Rebounds on China Strength, Supply Side Threats

Seaborne coal prices rebounded sharply this week, with the threat of strike activity in Colombia (which has seemingly been averted) pushing CIF ARA forwards up by the greatest extent. Further evidence of strength in Chinese electricity and coal demand were released this week, providing the market with considerable upside support. Despite the fact that the slowdown in China's demand from the Lunar New Year is looming, there is still several weeks of strong winter demand to get through, and buyers are likely still focused on ensuring adequate fuel supply. While the end of the labor strike threat in Colombia may pull down prices into next week, potential supply disruptions remain, particularly in the Pacific Basin, with the la Niña conditions potentially causing above normal rainfall in Australia and Indonesia over the next few months. This should keep prices supported into the New Year. However, if buyers can make it through the winter peak season unscathed following a year of largely unexpected growth in Chinese demand, 2Q and 3Q17 prices will face considerable downside pressure.

Soybean Resiliency

As traders become more and more impatient with the continuing resilience being exhibited in soybeans, more “negative” news last Friday and over the weekend has confounded the bears once again. On Friday, Brazilian agro-consultancy Safras & Mercado published a 106.1M MT production estimate, 4.1M MT above the December WASDE and 5M MT larger than PIRA.

U.S. Stock Excess Narrowing Resumes

Overall commercial stocks declined some 2 million barrels this past week compared to a 5 million barrel build the same week last year. This past week’s inventory decline was led by crude oil’s 2.6 million barrel drop even though Cushing crude stocks built 1.2 million barrels. Real product demand was not as weak as the EIA suggests, because of its inflated estimated exports. Next week PIRA sees another overall stock decline, this time led by distillates. Crude stocks are expected to show a small decline while Cushing builds.

Cash Prices Primed for Further Appreciation

Without the guarantee of cold weather ahead this season, it appears that erstwhile buyers might be having second thoughts about last week’s winter-time rally. To be sure, the market is making significant progress toward reversing the month-to-date gains, with the Jan’17 futures contract currently trading at $3.40/MMBtu or a W/W decline of ~$0.35. Moreover, the absence of “blue” weather forecast maps suggests the possibility that futures prices might be capped at $3.50/MMBtu until colder temperatures re-emerge in January.

Export Flows to Belgium/France Stay Strong; 1Q17 Dutch Prices Supported

German pricing has seen some increased volatility, with the baseload spot price having reached €60/MWh on Dec 14, a level not seen for the past 3 years. This is the result of low wind output (2 GW onshore and 600 MW offshore) and outages at coal plants, which has lowered the overall availability of conventional generation. The patterns of Dutch interconnector flows have also significantly changed versus the history, with the Dutch market turning overall in a net exporting position since September. Even if German flows to the Netherlands are restored to historically higher levels, the increased role of Dutch flows toward Belgium and France will still prevent downsides for the Dutch market.

Another Record Setting Week

The S&P 500 posted a record high on Tuesday and then spent the remainder of the week consolidating that peak. Financial stresses remain very low with ongoing low volatility. The U.S. dollar was generally stronger. On the commodity front, energy has remained strong, and precious metals have continued to give ground. The Cleveland Fed released their December report on inflation expectations, and there was a notable increase across all of the tracked maturities as the post-election reflation theme continues to play out in the market data.

Holiday Trade

With 10 days of trading left until 2017 and bearish fundamentals no matter where you look, it’s difficult to get too excited about the prospects of a year-end rally, although Fund money flow will have the ultimate say on that topic.

Additional New Regs Impacting Texas Coal

On December 9th, EPA proposed new requirements for Texas under the Regional Haze program. The rule would require significant upgrades at 8 coal-fired plants - similar to those in the previous Regional Haze rule for Texas, which EPA voluntarily withdrew last month after it had been stayed by the 5th Circuit Court. While these developments present a downside for Texas coal, PIRA anticipates that the new administration will not finalize the rule as proposed. This development is one of several Texas-specific rules issued as of late, including finalized SO2 nonattainment designations. EPA on December 14th also finalized a rule affecting the broader implementation of the Regional Haze program during 2018-28.

U.S. Ethanol Output Reaches Record High

U.S. ethanol production increased by 17 MB/D the week ending December 9 to a record 1,040 MB/D, eclipsing the previous high of 1,029 MB/D established earlier this year. Inventories built by 546 thousand barrels to 19.1 million barrels, though they are still 1.25 million barrels lower than this time last year. Ethanol-blended gasoline manufacture rose to 8,864 MB/D, rebounding from a ten-month low of 8,646 MB/D.

We're Go at Throttle Up

Japanese crude runs continued their rise as turnarounds wrap up. Crude imports fell back such that stocks drew 3.1 MMBbls. Finished products built a slight 0.3 MMBbls off their cyclical low. Compared to year-ago, the deficit on total commercial stocks was little changed at ~17 MMBbls, though the deficit on crude and finished products both widened slightly. Kerosene demand was much lower, as tertiary and secondary pull on primary inventory ebbed. The stock draw rate moderated, but the deficit relative to last year widened. Margins and cracks eased slightly on the week, and down from their November average.

Asian Price Strength Works its Way Back into Europe, but Is a Massive LNG Imbalance Looming in 2017?

The LNG market is falling into an intriguing trap if it does not pay attention; price support now is largely being caused by supply disruptions that are not necessarily sustainable. While it is possible that production problems will persist, it eerily reminds us of the crude oil price trap of 2014, when supply disruptions in the Mideast masked a significant surge in new supply emerging from North America.

A Glimpse of Winter Wonderland

In November, loads in the East fell by 1.7% year-on-year as heating degree days in the U.S. fell by 6%. However, ERCOT loads increased by 2.3% due to much above normal cooling demand. Stronger heating loads and higher gas prices are driving energy prices up year-on-year at all hubs in December. December Henry Hub is likely to average more than $1/MMBtu above November. However, PIRA expects adequate supply to keep a lid on gas prices. Despite the price gains, implied gas heat rates are down across the board and margins are weaker in most markets.

California Carbon Prices Mired below 2017 Auction Reserve Price

The 2017 Auction Reserve Price for CA has been set and the V-17 Dec-17 benchmark is averaging mid-way between the 2016 and 2017 ARPs. The Appellate Court decision in the auction lawsuit could come shortly following the January oral arguments date and will move the market; the CA Supreme Court will have the final say in 2017. Bidding interest in the Feb 22 auction could be diminished by a lack of news from the courts and a desire to “wait and see.” The Nov 2016 partial compliance surrender showed increased interest in offsets. Levels of offset usage will be a key driver of auction allowance demand (and allowance prices) under either legal scenario.

Global Equities Post a Mixed Week off Record Highs

Global equity markets posted a mixed week following the setting of record highs. In the U.S., among the key tracking indices, energy, consumer staples, and technology all outperformed and were little changed in an overall market that moved lower. Utilities gained on the week, while retail fell back the most. Internationally, pretty much all the tracking indices moved lower with noticeable weakness emanating from Asia and Latin America.

Winter Supply/Demand Fundamentals Converge in Japan to Support Price

In the coming weeks, Japan will take delivery of its first U.S. sourced cargo. Not coincidentally, the arbitrage between the U.S. Gulf and Asia has recently opened up to the point where even full cost recovery can be made- assuming that cargo is being sold at or near the levels being quoted for spot volumes in Asia of around $9.00/mmBtu.

UK Capacity Auction: 501 MW of Batteries Secure Contracts. Are Batteries Ready to Compete?

The third UK capacity market auction, completed on December 8, represented a milestone for battery storage systems – with 501 MW in batteries awarded contracts, or 10% of the 4.8 GW in total contracts for new capacity. The 28 successful batteries are all new-build assets and will use the 15-year contracts to finance their construction. However, PIRA’s analysis suggests that the final clearing price is insufficient to build and operate a li-ion battery economically, suggesting that operators will have to complement these contracts with significantly larger revenue streams.

Changes in Suez Canal Product Movements

Fuel oil movements southbound through the Suez Canal have declined since mid-2015 in response to lower Russian fuel oil exports out of the Black Sea. Middle distillate movements northbound have increased over the same period, mainly because of additional Middle East refining capacity. Gasoline movements northbound are down slightly.

3Q16 U.S. Producer Survey: Shale Production Engine Stalls on Price

Confirming our early guidance of shale production declines in 2016, the 3Q16 U.S. Producer Survey reveals a year-on-year loss for the reporting group — notably, the first decline since the surge in shale production began in 2008. Given the relative weighting of the Survey (toward those companies active in unconventional plays), the retrenchment speaks volumes about the depth that prices have fallen this year. In contrast to prior quarters, U.S. production activity during the reporting period was defined by stagnation in the Appalachian basin — a region which has consistently offset declines occurring in other basins.

U.S. Crude Exports Driven by Regional Arbitrage Incentives

In December 2015, the U.S. government repealed restrictions limiting the export of U.S. crude oil. Until then, Canada was the only significant exception to the rule and exports to Canada averaged 430 MB/D in 2015. Since easing trade limitations, the range of destinations has broadened, though Canada still continues to serve as a major recipient of U.S. crude. Over the ten-month period from January to October 2016, Canada accounted for 60% of U.S. crude exports, followed by Europe at 20%, Latin America at 10%, and Asia at 10%.

Asian Demand Growth: Good Growth, but Slight Ease

PIRA's latest update of major country Asian product demand shows growth remaining strong, though there was some easing in the latest snapshot. Our latest assessment of growth is now 800 MB/D versus year-ago. Versus the assessment last month, there was noted slowing of growth in China and India, which remain the key drivers. In China, gasoline demand remains strong and dominates performance in Asia, supported by strong car sales and signs of economic reacceleration in latest Chinese data.

Libyan Oil Increases Possible, But Watch for More Conflicts

PIRA sees some chance that Libyan oil exports will start to rise in the coming weeks, following the Zintani militias’ agreement to end their blockade of key western pipelines. However, any gains remain highly uncertain and, in our view, unsustainable. Local militias currently control the Sharara and El Feel fields that feed the pipelines to the Mellitah and Zawiya western export terminals, and they are embattled in their own conflict. Fighting is likely to break out and disrupt any production increases. We may also see Ibrahim Jathran (head of the facilities guards that lost control of the main eastern terminals to Khalifa Haftar) get involved with more counterattacks.

Will Lifting of Sanctions Increase Russian Oil Production?

The impending Trump administration is likely to push for better relations with Russia which could result in the lifting of sanctions. Even if the efforts are successful, it will take time before significant additional production either from shale oil or from the Artic comes to market. Shale oil is likely to be developed faster than the Artic. But Russian shale remains in its infancy and it will take time to build up sufficient drilling and completion infrastructure, and achieve significant cost reductions. Russian Arctic development will likely take much longer due to higher costs, logistics and environmental concerns. Even if sanctions are lifted, long lead times between discovery and production suggest significant new Arctic volumes are not likely for another 8-10 years.

December Weather: The U.S., Europe, and Japan Cold

At mid-month, December looks to be 3% colder than the 10-year normal for the three major OECD markets, bringing the month oil-heat demand to 120 MB/D above normal. On a 30-year-normal basis, the markets are 2% warmer.

Tight U.S. Labor Market Poses Challenge for Drilling Activity

U.S. mining sector employment boomed during the 2010–2014 period (increasing by roughly 220,000 jobs, or 35%), as oil production rose substantially. Slack in the labor market made it easy to fill drilling jobs in this period – coming off the 2008–2009 recession, the national unemployment rate was almost at 10% in early 2010. In the last two years, mining shed jobs at a fast pace as lower oil prices and a collapse in rig counts took their toll. But the overall labor market performed well and the unemployment rate came down to a historically low level of 4.6% last month. With low unemployment, increasing drilling activity will very likely result in wage pressure, raising the cost of producing shale crude.

Iraq Oil Monitor, 4Q16

It is unclear whether Iraq will implement the November 30 agreed cut of 210 MB/D because of an internal conflict between Baghdad and the South Oil Company. PIRA expects the export agreement between the KRG and Baghdad to hold through 2017, but northern security risks will persist long after the expulsion of ISIS. Irregular export payments prompted warnings of lower investment from operators in Kurdistan, where former Baghdad-controlled fields account for an increasing share of oil production. In the south, contract negotiations continue with operators, delaying targeted production ramps.

The information above is part of PIRA Energy Group's weekly Energy Market Recap - which alerts readers to PIRA’s current analysis of energy markets around the world as well as the key economic and political factors driving those markets.

"As a result of closing this transaction, Anadarko now operates the largest number of floating production facilities in the deepwater Gulf of Mexico, which provides a competitive advantage to leverage this infrastructure into attractive new investment opportunities," said Anadarko Chairman, President and CEO Al Walker. "This region continues to play a key role in our portfolio by contributing to our higher-margin oil growth profile, while generating substantial future free cash flow to accelerate the growth of our world-class U.S. onshore assets in the Delaware and DJ basins. The expanded portfolio of deepwater facilities provides numerous hub-and-spoke opportunities that can generate rates of return of better than 50 percent at today's prices. Given our industry-leading capabilities in deepwater project management, production solutions and exploration success, adding these high-quality assets greatly improves our ability to deliver strong performance in a volatile commodity environment."

"As a result of closing this transaction, Anadarko now operates the largest number of floating production facilities in the deepwater Gulf of Mexico, which provides a competitive advantage to leverage this infrastructure into attractive new investment opportunities," said Anadarko Chairman, President and CEO Al Walker. "This region continues to play a key role in our portfolio by contributing to our higher-margin oil growth profile, while generating substantial future free cash flow to accelerate the growth of our world-class U.S. onshore assets in the Delaware and DJ basins. The expanded portfolio of deepwater facilities provides numerous hub-and-spoke opportunities that can generate rates of return of better than 50 percent at today's prices. Given our industry-leading capabilities in deepwater project management, production solutions and exploration success, adding these high-quality assets greatly improves our ability to deliver strong performance in a volatile commodity environment." OPEC Deal, Trump Election Boost Industry Outlook

OPEC Deal, Trump Election Boost Industry Outlook

With OPEC Delivering on Cuts, Prices to Move Higher

With OPEC Delivering on Cuts, Prices to Move Higher U.S. Commercial Stocks Led Lower by Product Draw

U.S. Commercial Stocks Led Lower by Product Draw

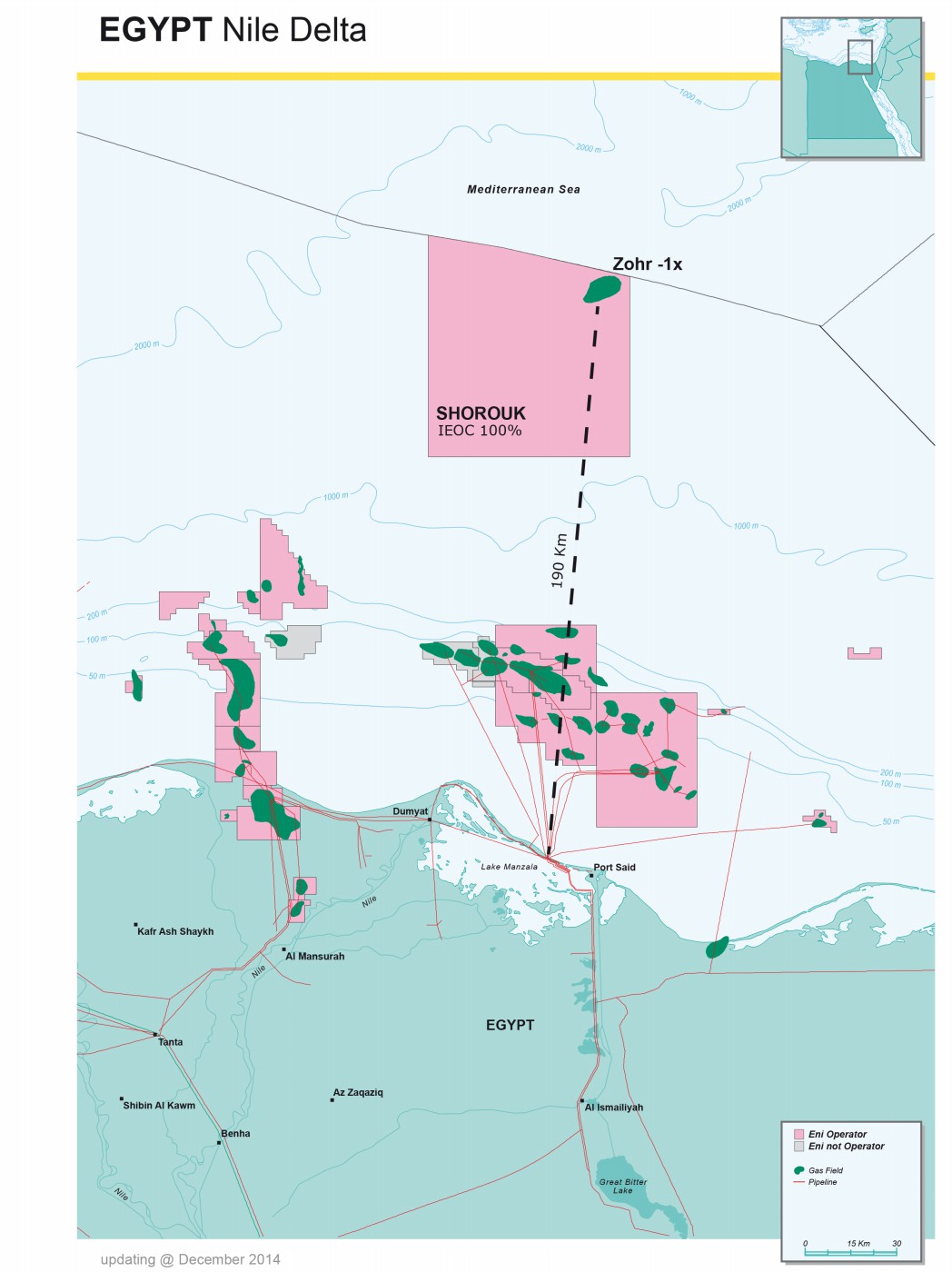

Eni has agreed to sell to BP a 10% participating interest in the Shorouk Concession, offshore Egypt, where the supergiant gas field Zohr is located. Eni, through its subsidiary IEOC, currently holds a 100% stake in the block.

Eni has agreed to sell to BP a 10% participating interest in the Shorouk Concession, offshore Egypt, where the supergiant gas field Zohr is located. Eni, through its subsidiary IEOC, currently holds a 100% stake in the block.

Asia's Refinery Cracking Capacity Additions Slowing, but India Continues to Upgrade

Asia's Refinery Cracking Capacity Additions Slowing, but India Continues to Upgrade Gasoline Strength Supporting Refining Margins

Gasoline Strength Supporting Refining Margins