Crude Oil:

The Red Queen and Alice discussed the problems of running and making progress in Alice in Wonderland. “‘Well, in our country,’ said Alice, still panting a little, ‘you'd generally get to somewhere else—if you run very fast for a long time, as we've been doing.’”

“‘A slow sort of country!’ said the Queen. ‘Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!’"

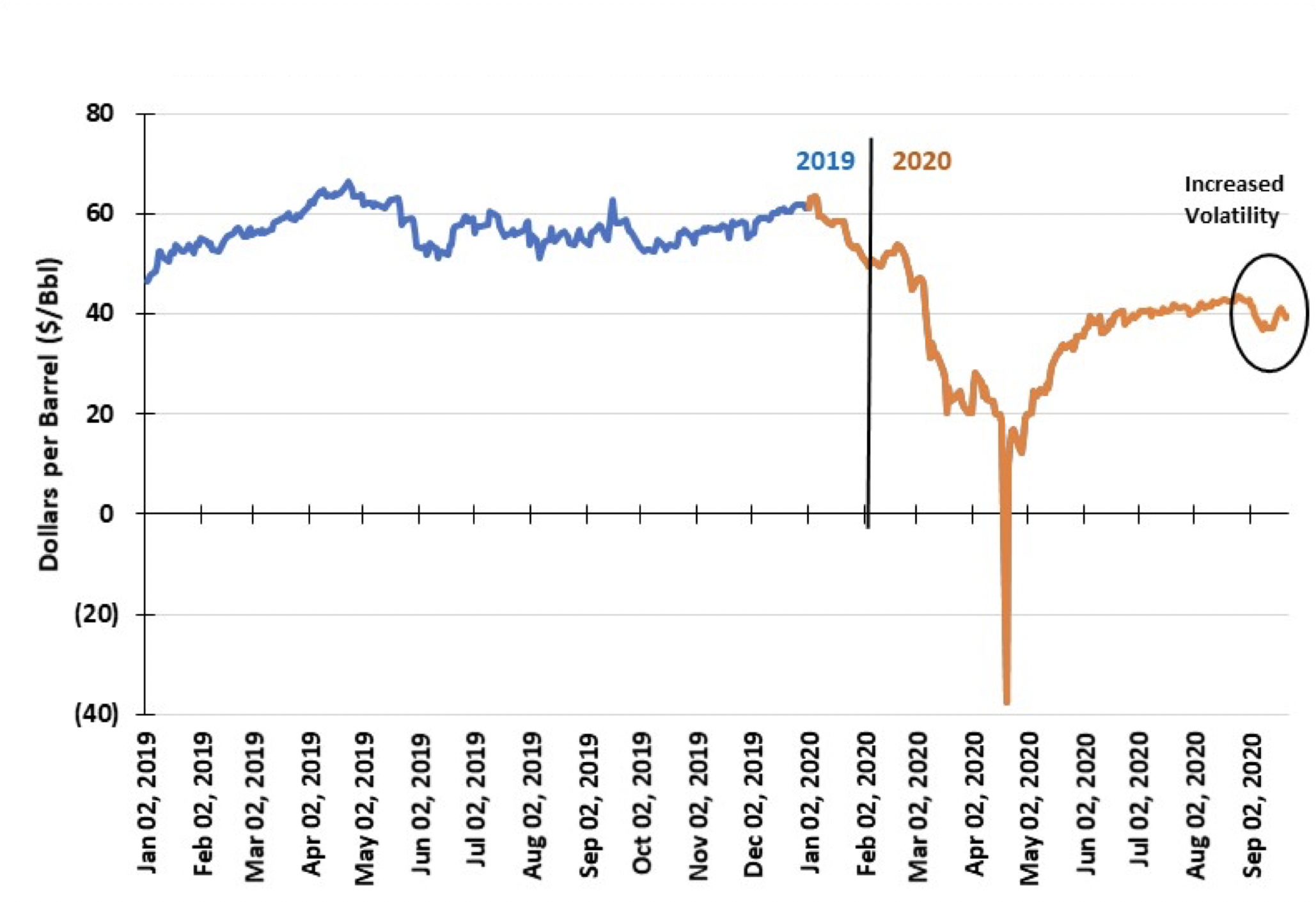

That may describe crude oil prices since they rebounded following the devastating demand collapse in March and April. After falling in late April to a negative $39 per barrel, oil prices rebounded to $40 by early June. Since then, like the Red Queen, the oil market has been running hard only to remain in the same place.

That may describe crude oil prices since they rebounded following the devastating demand collapse in March and April. After falling in late April to a negative $39 per barrel, oil prices rebounded to $40 by early June. Since then, like the Red Queen, the oil market has been running hard only to remain in the same place.

In the past several weeks, as new COVID-19 outbreaks emerged in Europe and various U.S. states, oil demand’s anticipated recovery has been called into question. With OPEC and its partners discussing adding more supply to the global oil market, and U.S. producers restarting wells suspended last spring, prospects of a second half 2020 oil glut have grown, poisoning the oil market sentiment. The souring outlook for an improvement in the supply/demand balance knocked oil prices down from $45 a barrel to $38.

Recent commentary from the heads of three of the world’s largest oil trading firms reflects sharply differing outlooks, helping explain why oil prices are stuck around $40. Two trading houses see demand weakening and supply growing. They see global oil inventories rising to the point we will see oil tanker storage becoming popular again. The largest trading firm sees China oil demand recovering to previous levels, more airplanes flying and mobility picking up. Therefore, they see global oil inventories shrinking, supporting higher oil prices. A recent Dallas Federal Reserve Bank survey of oil executives concludes that they will end 2020 between $40 and $45 a barrel—more running in place.

The market’s optimism/pessimism struggle will not be resolved soon. Only additional data will establish the direction. As government leaders are learning, their constituents will not tolerate lockdowns for much longer. We know the most vulnerable people in society at risk of the virus and how to protect them. By practicing healthy protocols, there is little reason why economies cannot become more open. Fear of the disease will keep the recovery in activity restrained, but it likely won’t halt it. Total confidence will only come with a vaccine, but a more normal life can be lived in the meantime. Better oil demand lies ahead.

Natural Gas:

Natural Gas:

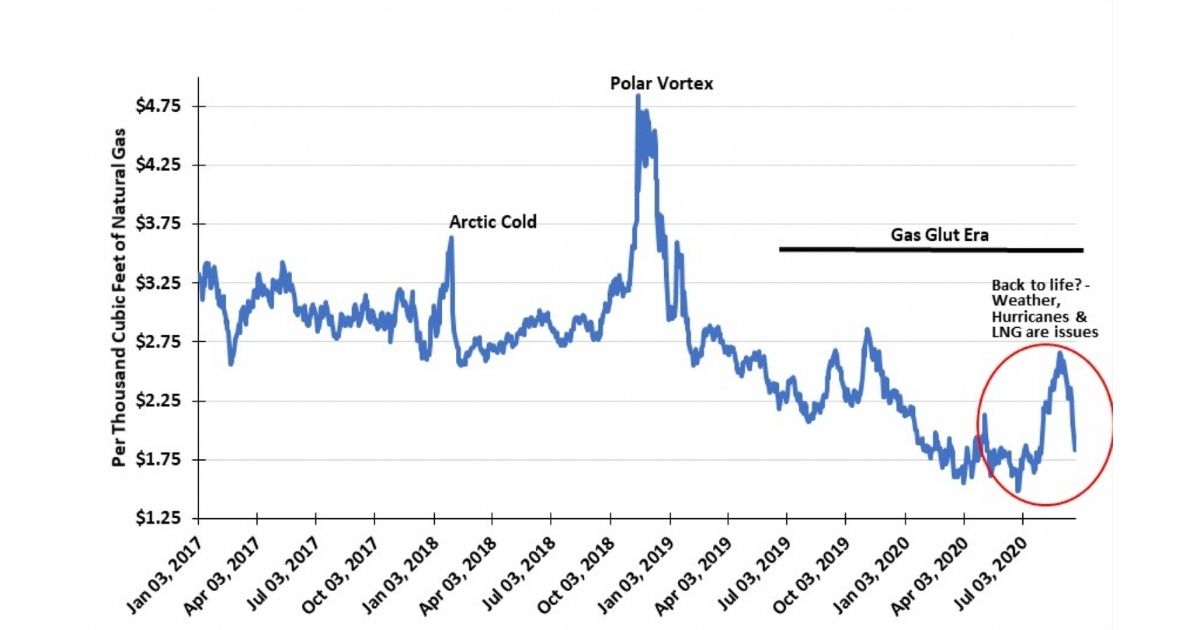

We suggested in our last column that weather and LNG shipments would control natural gas pricing. Both dynamics have impacted gas prices and are continuing to impact them, increasing price volatility. The latest disrupter is the fallout from hurricanes hitting the Gulf Coast and cutting natural gas demand. While the storms played their usually havoc with offshore gas production, it has been the devastation of the Lake Charles region of Louisiana by Hurricane Laura that has had the greatest demand impact. The storm created weeks-long power outages, shutting down several LNG export terminals.

The idled LNG terminals forced them to curtail their gas feed. The curtailments have added to the supply glut, which, not surprisingly, caused a sharp drop in spot gas prices. Spot gas prices fell substantially more than futures prices. That was not surprising, as all prices needed to adjust to a level that would entice buyers into the market. Some analysts interpreted the spot price drop, which bottomed at $1.33 per thousand cubic feet, as establishing a new trend for the overall gas market, rather than a one-time event driven solely by the speed with which the glut emerged.

Besides the hurricane’s impact on LNG shipments, weather-related demand also disrupted the market. Temperatures rapidly went from unseasonably hot to unseasonably cold and then back again. When the air conditioning power load evaporated, support for gas prices eroded. The cold temperatures, while unseasonably cool, were insufficient to generate a meaningful uptick in heating-related gas consumption. This was just one more slam to gas demand, which forced prices to adjust to properly allocate gas supply.

The optimism that natural gas supply would drop as crude oil production fell in response to weak oil prices has not been as strong as the reality that demand has fallen more than gas output. Associated natural gas supply has declined, and will likely continue declining, as long as oil drilling doesn’t pick up soon. With oil prices predicted to remain below the level that would restart drilling activity, associated natural gas supply should contract further during 2021.

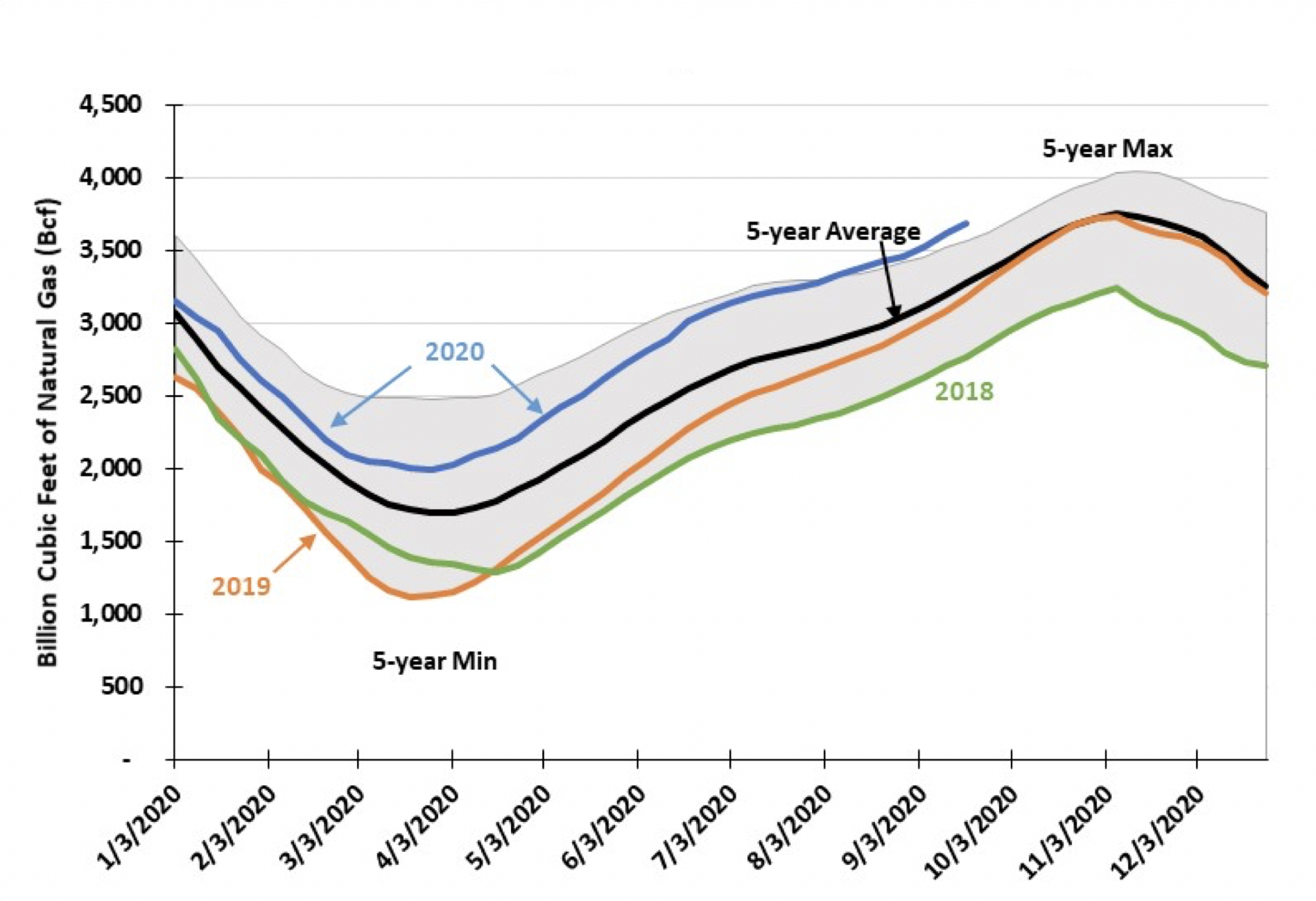

The key issue for gas prices will be, as it always is at this time of the year, the expected level of storage when winter ends. As the current gas inventory shows, there is more gas in storage than during the past five years. Should we experience another warm winter, such as those of the past two, gas storage next April is likely to be greater than normal. Absent soaring demand for power generation and/or LNG exports, gas prices will face headwinds this winter and next summer.

By G. Allen Brooks | Author, Musings From the Oil Patch