As the climate is changing, the Arctic is warming four times faster than global averages, causing the circumpolar Jetstream to weaken and move southwards. Consequently, freezing cold air masses – known as the Polar Vortex – descend to more densely populated areas in the earth’s Northern Hemisphere, where humans have no other immediate choice but to increase fossil fuel consumption to keep warm.

Analyzing global temperatures and related weather phenomena, Rystad Energy believes that the increased frequency of this weather pattern – which has caused a rise in demand for coal, liquefied natural gas (LNG), electricity and even a bit of oil – is here to stay. Recent eye-popping price spikes and their spread between summer and winter will widen, especially for gas, both natural and liquefied.

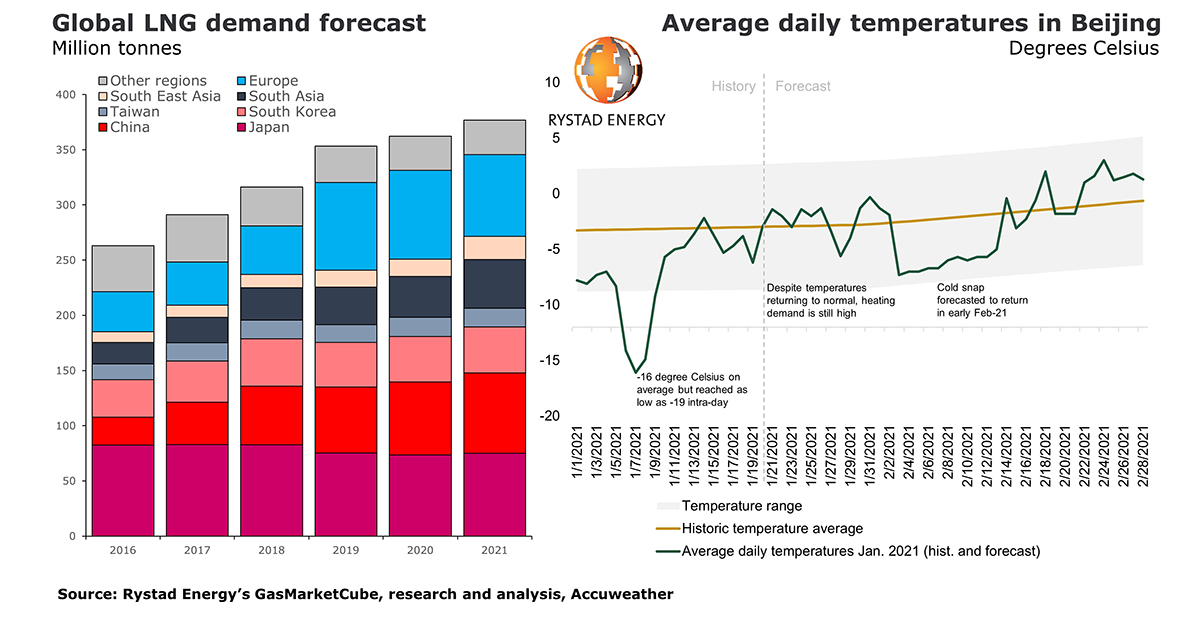

With European and Asian markets hungry for natural gas and LNG, storage levels are getting depleted. And with the Polar Vortex expected to create another cold snap in February, a perfect demand storm will likely cause a spike in global demand and contribute to a 4% rise in LNG consumption this year, reaching about 377 million tonnes (MT) in 2021 versus 363 MT in 2020.

Due to the cold snap, North-east Asia has already reached an international LNG import all-time-high in December, when the region imported a record 22 MT. China in particular imported a record 66 MT in the whole of 2020, despite the effect of the Covid-19 pandemic, and is on the verge of overtaking Japan as the world’s largest LNG importer. Rystad Energy expects Chinese LNG imports in 2021 to grow to 72.9 MT, just 2 MT short of Japan’s projected 74.9 MT.

The Polar Vortex has so far hit Asian and European markets hard, causing a rise in the profitability of LNG, natural gas and coal. Rystad Energy’s price forecasts show that high gas and LNG price levels will likely remain high in coming weeks and are only likely to ease back in March and April as spring approaches in the Northern Hemisphere.

Yet US Henry Hub gas prices remain surprisingly subdued at $2.75 per MMBtu, a steep drop from the peak price of $3.40 per MMBtu registered in late October 2020. There are two main reasons US gas prices are comparatively depressed. First, the Polar Vortex has so far only drifted south over Europe and Asia, and not yet North America. Second, higher oil prices are incentivizing shale operators to tap into drilled but uncompleted wells (DUCs), which increases the domestic supply of both oil and gas.

As more wells are brought online, we see continued pressure on domestic US gas prices, even despite the surge in demand for US LNG exports. Rystad Energy expects the Henry Hub price to average $2.95 per MMBtu in 2021, in nominal terms.

The Polar Vortex, together with increased North East Asian demand for heating, has pushed up Asian LNG prices and the arbitrage window between the US and Asian markets. This has directed more US LNG volumes to the Far East compared to the US and Europe. Consequently, the long voyage from source to market is good for vessel demand, and thus also charter rates.

The increased demand for US LNG in Asia has led to congestion in the Panama Canal, the shortest route for transporting LNG from the US Gulf Coast to Asia. Maintenance and weather disruptions have further supported the current backup in the canal. Consequently, shippers may have to use alternative routes including passing through the Suez Canal or around South Africa for transporting cargoes from the US to Asia.

These routes would more than double the route distance and increase passage time from 20 to 30 days. As such, voyage costs for cargos from the US to Japan have soared as high as $5.60 per MMBtu during January 2021.

Perfect storm for coal

Japan presents an interesting case of how the attractiveness of coal has rebounded as a result of the Polar Vortex. With most of Japan’s nuclear reactors still offline in the wake of the Fukushima disaster, Japan has relied heavily on LNG to meet its power demand and is therefore vulnerable to any shock related to the supply and demand balance in the LNG market. The Japanese power sector has also been affected by heavy snowfall and a lack of sunshine, thus affecting solar power generation and worsening the overall power supply. While the shortage can be offset by increased use of coal and oil, utilities have asked the public to use less electricity, a difficult ask in the midst of freezing temperatures.

The situation is hardly better in China. On 7 January 2021, Beijing recorded its lowest temperature since 1966 – touching -19.6 degrees Celsius. This has sharply lifted Chinese coal demand for both heating and power, and to deal with the demand spike, major north Asian energy consumers have ramped up coal consumption in recent weeks. In particular, thermal coal spot prices in China have soared since the start of the new year.

The cold weather has dampened domestic coal production and transportation, though the nationwide coal shortage started to appear in early November when major domestic coal-producing areas in Inner Mongolia, Shaanxi and Shanxi provinces reported reduced supply due to the government’s crackdown on illegal production and sale of coal.

But the volatile coal market situation has also been exacerbated by the government’s own policy decisions. China's coal import quota system, plus the informal ban on Australian coal imports, has resulted in limited imported coal available to take up the domestic production shortfall, even though it is substantially cheaper. Chinese coal buyers were able to increase imports from Indonesia and Russia in December as the annual quota expanded, and have also recently turned to alternative sources of supply, including South Africa and Colombia, but these volumes are reportedly unlikely to arrive in time or in sufficient quantities to meet short-term demand requirements.

“The new round of lower temperatures can support the high energy prices in the market. As milder weather returns, we expect to see less upward pressure on energy prices. Still, the market will continue to be tight during the coming months, as challenges in the Panama Canal are yet to be resolved, Chinese coal production needs to recover, and gas storage needs to be restocked for the current market tightness to ease,” says Sindre Knutsson, vice president of gas market research at Rystad Energy.

For more analysis, insights and reports, clients and non-clients can apply for access to Rystad Energy’s Free Solutions .

Source: Westwood Analysis")