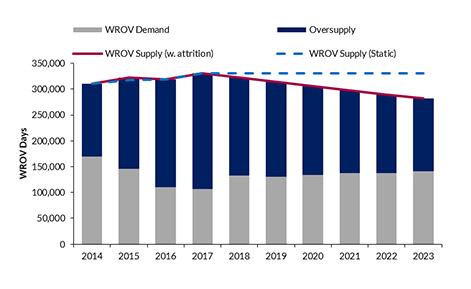

Westwood estimates 2017 global utilization reached a low of 32%, down from 55% in 2014.

Top-tier ROV operators Oceaneering and Helix Energy Solutions quoted 2017 utilization of 46%, and 42%* respectively. Over the forecast, the oversupply situation will ease, with utilization levels expected to return to 50% by 2023. Whilst stable demand growth is forecast (2% CAGR), ROV expenditure is constrained at present by a slow recovery in day rates in what remains a ‘buyers market’. As utilization improves, ROV operators can expect to see commercial terms moving in their favor.

The latest edition of Westwood’s World ROV Operations Market Forecast is now available. The market for work-class ROVs (WROVs) is fundamentally tied to the offshore oil & gas sector which is exiting a cyclical downturn and now entering a period of recovery. Cost efficiency remains critical and drives the need for modern systems that can maximize uptime. Demand for both traditional oil and gas applications and new offshore support roles will support a recovery in demand over the 2019-2023 forecast.

Westwood estimates 2017 global utilization reached a low of 32%, down from 55% in 2014. Top-tier ROV operators Oceaneering and Helix Energy Solutions quoted 2017 utilization of 46%, and 42%* respectively. Over the forecast, the oversupply situation will ease, with utilization levels expected to return to 50% by 2023. Whilst stable demand growth is forecast (2% CAGR), ROV expenditure is constrained at present by a slow recovery in day rates in what remains a ‘buyers market’. As utilization improves, ROV operators can expect to see commercial terms moving in their favor.

Global WROV Supply-Demand Balance 2014-2023

*Robotics segment includes remotely operated vehicles (“ROVs”), trenchers and ROVDrills.

Key Conclusions:

Key Conclusions:

- WROV utilization to recover from 2017 lows, but not expected to reach pre-downturn levels. Oversupplied market to be eased over the forecast.

- Global ROV demand to total 680,917 days over 2019-2023, growing at a 4% CAGR off the back of improved market conditions. Expenditure to total $6.9bn over the forecast.

- Drilling support to be largest ROV market accounting for 40% of total expenditure, growing at 6% CAGR. The sector will lead by Latin America with activity in Brazil, Guyana and the Falkland Islands bolstering demand.

- IMR support demand to increase 11% and expenditure to total $2.2bn over forecast, driven by an ageing installed base of infrastructure.

- Increased autonomy remains a goal for ROVs, with operations aimed at requiring less manned intervention.

- Subsea resident ROVs (RROVs) remain a long-term goal for oil & gas operators, as developments are sanctioned in ever more challenging and remote locations.

For the latest update of World ROV Operations Market Forecast, Westwood has undertaken new analysis on the supply-demand balance and utilization of work-class ROVs.