Crude Oil

By G. Allen Brooks | Author, Musings From the Oil Patch

By G. Allen Brooks | Author, Musings From the Oil Patch

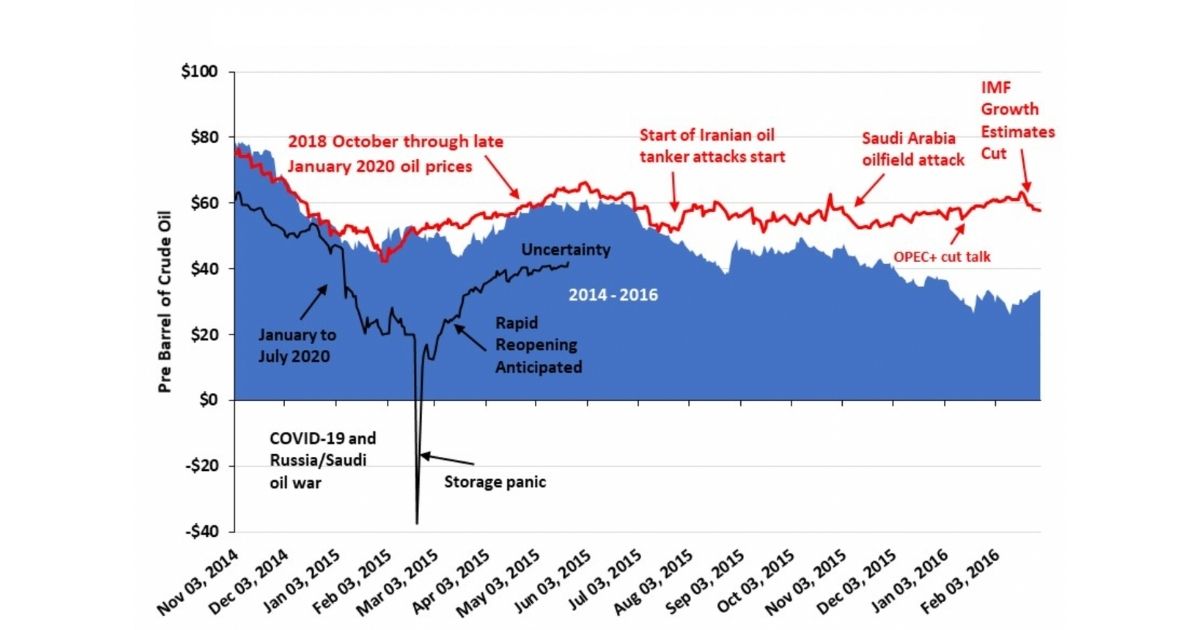

The last time we commented on the state of commodity markets, we discussed the oil market showing signs of improvement following the oil price’s journey into negative territory. At the time, we wondered how far the recovery might go. Since then, we watched market forces pushing oil prices higher overwhelm those tugging them lower. The trajectory of oil prices remains uncertain, as everything seems to revolve around the health (pardon the pun) of the coronavirus.

As various U.S. states reopened their economies last May, believing they had “flattened the curve” of infections, economic activity quickly rebounded. The surges in daily road traffic and pickups in air flights convinced refiners to restart operations, drawing from the vast stores of crude oil that had built during the shutdown. Speculation swirled around whether the “V-shaped” oil demand rebound would continue, or possibly falter. The rising activity lifting oil demand also inflated future expectations for growth, pushing oil prices to $40 a barrel, where they currently sit, but doubts about a further rise are growing.

The surprising June surge in virus infections in many early-opening states has forced pauses or retreats in those openings, choking off activity. The virus surges have undermined optimism about how strongly the U.S. economy is rebounding, as fear of the illness has paralyzed reopening initiatives. The result has been a flattening, and, in some case, actual declines, in traffic data in many of the states rolling back their openings, indicating less oil use.

The oil price recovery emboldened OPEC+ to ease its production cutback. As the organization’s members watch U.S. oil production fall, both due to wells being shut-in and the absence of new wells coming into production, OPEC+ seems intent to boost its output in line with anticipated global demand increases. OPEC+ is trying to regain the market share lost to the U.S. in recent years. One wonders how soon internal battles over OPEC+ production quotas erupt, and what that might do to supply growth. Given the precariously balanced market, uncertainty over the pace of oil supply and demand growth in the face of existing high global oil inventory levels makes navigating the future a challenge. We could just as easily see another crushing blow delivered to oil prices, as a spike to $100 a barrel. Each outlook is associated with wildly different outcomes. Like the three bears story, we’re really hoping for: "Ahhh, this porridge is just right."

The oil price recovery emboldened OPEC+ to ease its production cutback. As the organization’s members watch U.S. oil production fall, both due to wells being shut-in and the absence of new wells coming into production, OPEC+ seems intent to boost its output in line with anticipated global demand increases. OPEC+ is trying to regain the market share lost to the U.S. in recent years. One wonders how soon internal battles over OPEC+ production quotas erupt, and what that might do to supply growth. Given the precariously balanced market, uncertainty over the pace of oil supply and demand growth in the face of existing high global oil inventory levels makes navigating the future a challenge. We could just as easily see another crushing blow delivered to oil prices, as a spike to $100 a barrel. Each outlook is associated with wildly different outcomes. Like the three bears story, we’re really hoping for: "Ahhh, this porridge is just right."

Natural Gas

Natural Gas

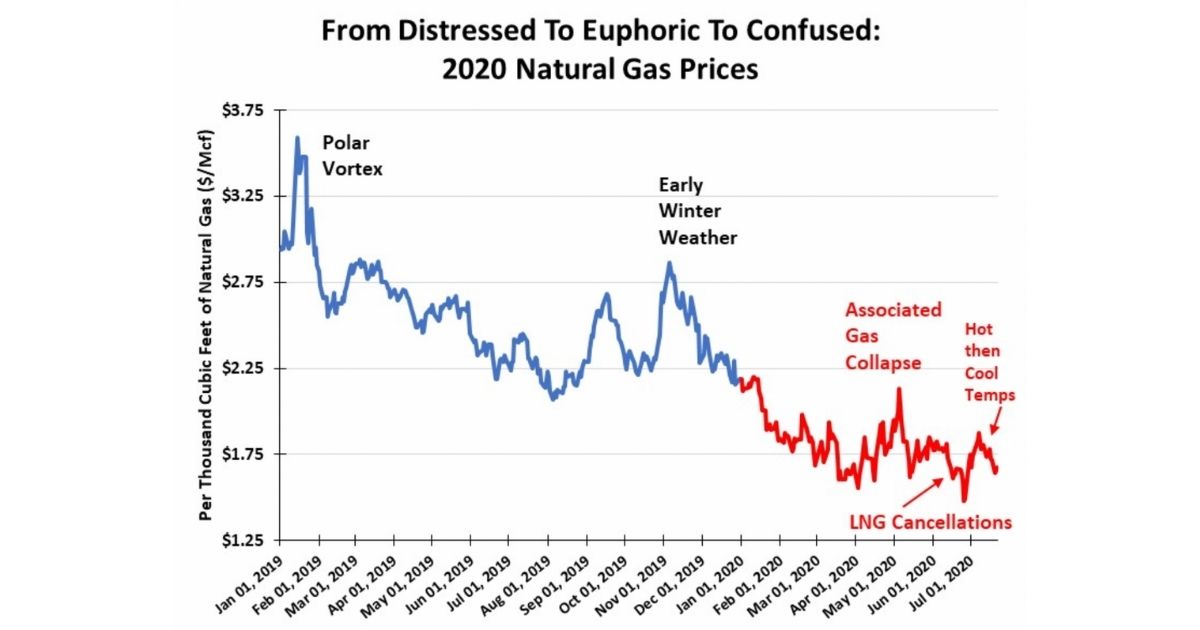

Our last missive stated that natural gas prices were at the mercy of weather and LNG shipments. The latter, a significant natural gas demand driver in recent years, and the impetus for substantial capital investment in the industry, had been in control of gas prices until the past few days, as hot temperatures have taken over driving gas prices.

The underlying market driver has been the anticipated fall in associated natural gas from shale oil wells. That supply has only recently begun showing signs of decline, something that is anticipated to impact future gas supply and lift prices. According to EIA data, shale output between December 2019 and June 2020 has declined by 4 Bcf/d, or -5.5 percent, probably indicative of the drop in total U.S. gas supply.

The price recovery from less gas supply has been overwhelmed by the cancellation of a large number of LNG export shipments. The fate of the U.S. LNG business is tied to global natural gas prices. The growth of the LNG business has been keyed to low wellhead prices that made domestic gas highly competitive in the global market. Early in the LNG export era, global gas prices were in double-digits, with U.S. prices in single-digits. The U.S.-global price spread provided substantial profits to cover gas liquefication and transportation costs. That business model began unravelling when global prices fell into mid-single-digits due to surging international gas supplies. While sub-$2 per Mcf U.S. wellhead prices continued to support LNG economics, recently, global gas prices converged with Henry Hub prices, destroying those economics.

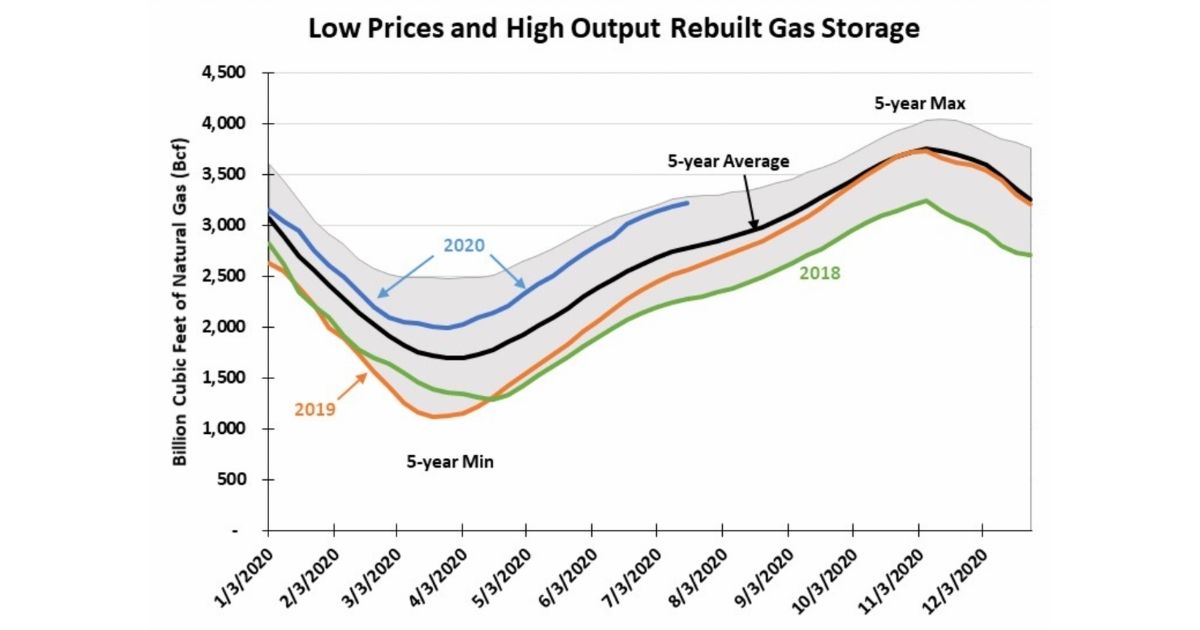

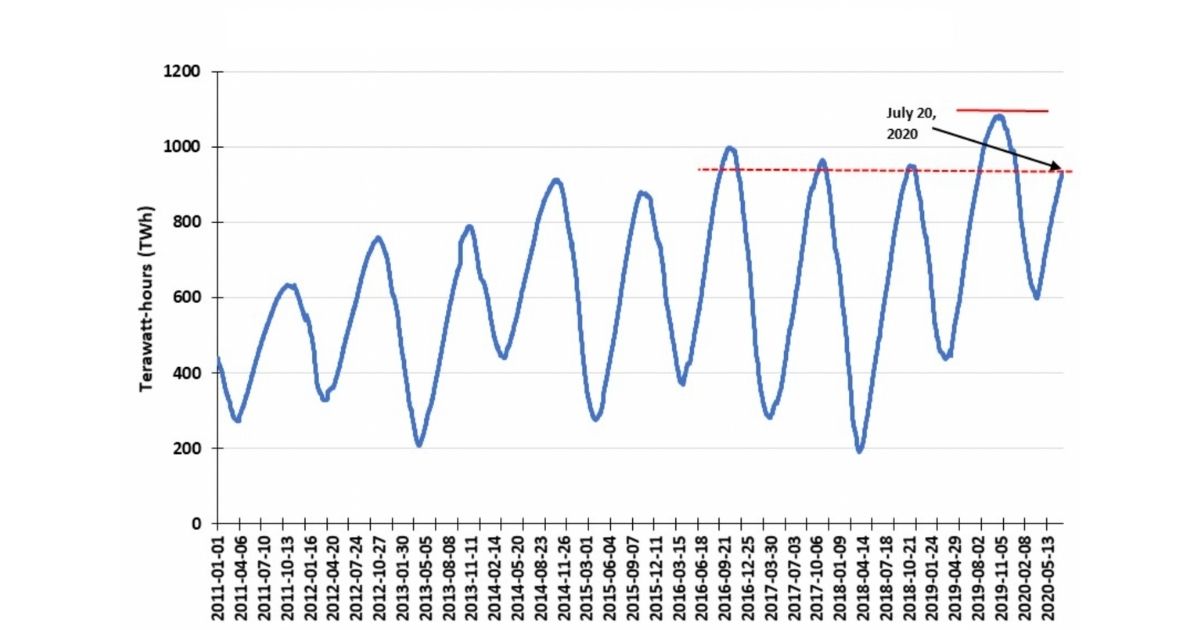

Global gas prices converged on U.S. prices due to surging supplies. That supply growth, coupled with warm winters, left above-average gas volumes in storage, depressing prices. This has been particularly true in Europe, which was a target market for U.S. LNG cargoes. Europe has new pipeline supplies coming from Russia, a supply source that is anticipated to grow. Last winter, European gas storage reached an all-time peak. As of mid-July, European gas storage is heading towards matching last year’s record. It is already at levels comparable to the peak volumes reported during the 2016-2018 winters. In other words, Europe is swimming in natural gas.

Global gas prices converged on U.S. prices due to surging supplies. That supply growth, coupled with warm winters, left above-average gas volumes in storage, depressing prices. This has been particularly true in Europe, which was a target market for U.S. LNG cargoes. Europe has new pipeline supplies coming from Russia, a supply source that is anticipated to grow. Last winter, European gas storage reached an all-time peak. As of mid-July, European gas storage is heading towards matching last year’s record. It is already at levels comparable to the peak volumes reported during the 2016-2018 winters. In other words, Europe is swimming in natural gas.

The convergence of global gas prices has pressured U.S. LNG sellers to cancel cargoes. From May through September, nearly 150 LNG cargoes have been cancelled. Encouragingly, the number of September cargo cancellations is half the average monthly cancellations of June to August. Fewer cancellations reflect the recent uptick in natural gas futures prices for the early months of 2021 in Europe and Asia. The increase in international gas prices is outpacing the rise in U.S. gas futures, widening the price spread, which will restore LNG profitability.

Optimism for higher natural gas prices is growing, based on expectations for falling gas supply and rising demand due to more power generation use and increased LNG exports. Both price drivers need to be watched closely, as they are likely to be more volatile than in the past.

By G. Allen Brooks | Author, Musings From the Oil Patch